DXY Technical Outlook

It’s extremely difficult to untangle the dollar from the euro in the third quarter as the single currency makes up 57.6% of the US Dollar index’s (DXY) composition. This means the dollar could consolidate or even exhibit weakness against other major currencies and still rise if the euro weakens substantially. Therefore, DXY remains vulnerable to a move higher, particularly at the very start of the quarter as the French go to the polls. Thereafter, the remainder of the quarter could see the greenback drift lower if that first- rate cut comes into view.

The DXY chart below shows the US-German 10-year bond spread which typically guides the pair. The interest rate differential suggests the dollar is overvalued or the euro is undervalued as the last time the bond spread was 1.87% the index traded at the 102.25. The price at the time of writing is 105.75. There is scope for the dollar to first strengthen before weakening later in the forecast horizon.

US Dollar Basket Weekly Chart

Source: TradingView, prepared by Richard Snow

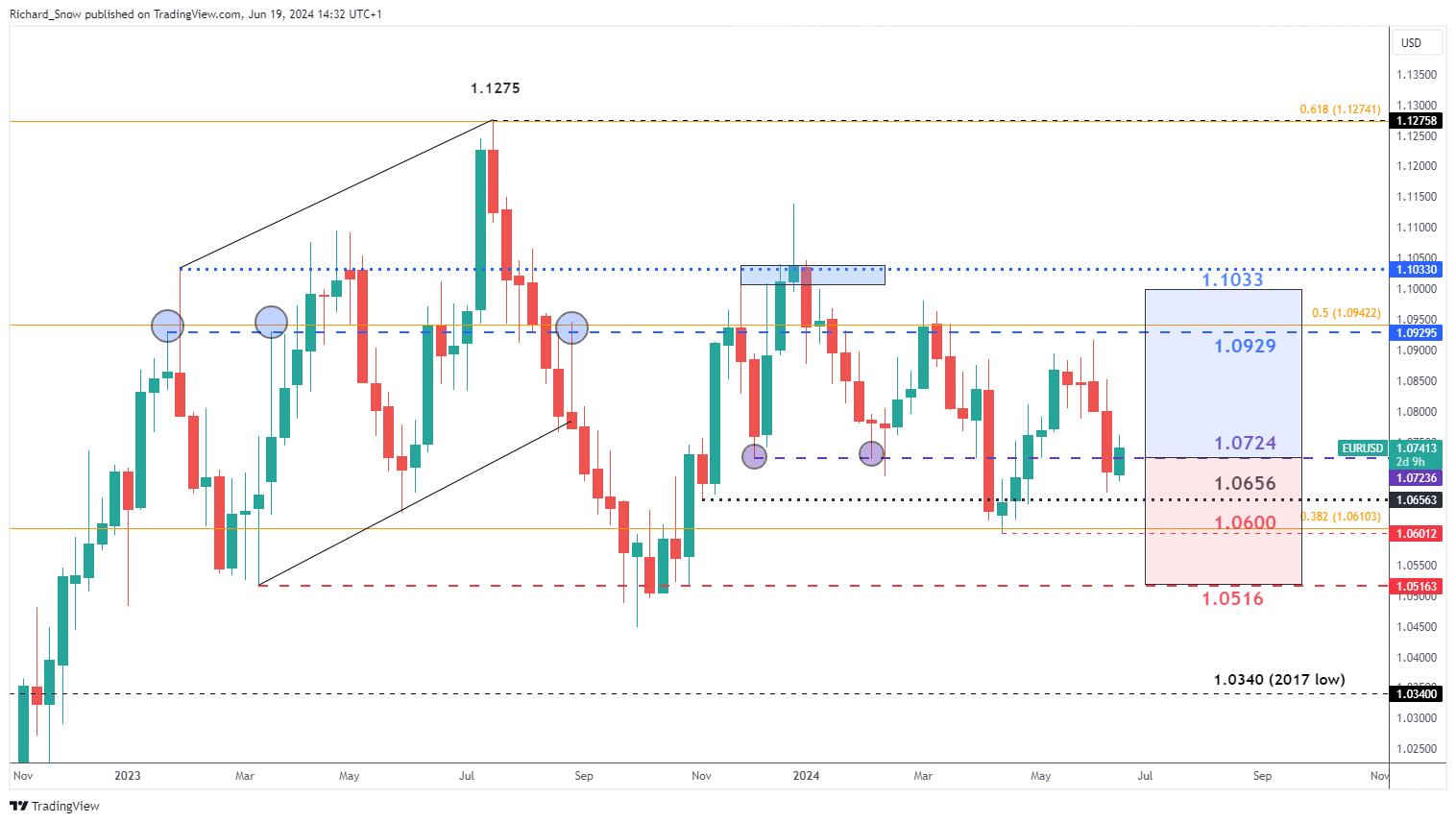

EUR/USD to Feel the Weight of French Elections but a Recovery is in View

EUR/USD has exhibited a broad, choppy downtrend for 2024, moving back and forth in a reactive fashion as rate cut projections were clawed back significantly in the US and to a lesser degree for the ECB; hence the pair favouring the downside. The euro may see some recovery in Q3, but uncertainties persist as concerns over French elections clash with Fed easing policies. The Fed's actions are expected to be the primary influence, even if the euro fails to show significant strength against other G7 currencies.

1.0600 may come into play if the spillover from the French elections’ filters across European bond markets. Potentially even bringing 1.0516 into view. Thereafter, should the Fed signal a much-improved possibility of that first rate cut materializing in Q3, the pair may head towards 1.0929 and potentially above the 1.1000 psychological level at 1.1033.

EUR/ USD Weekly Chart

Source: TradingView, prepared by Richard Snow

After acquiring a thorough understanding of the technical landscape for the US dollar in Q3, why not see what the fundamentals suggests by downloading the full US dollar forecast for the third quarter?

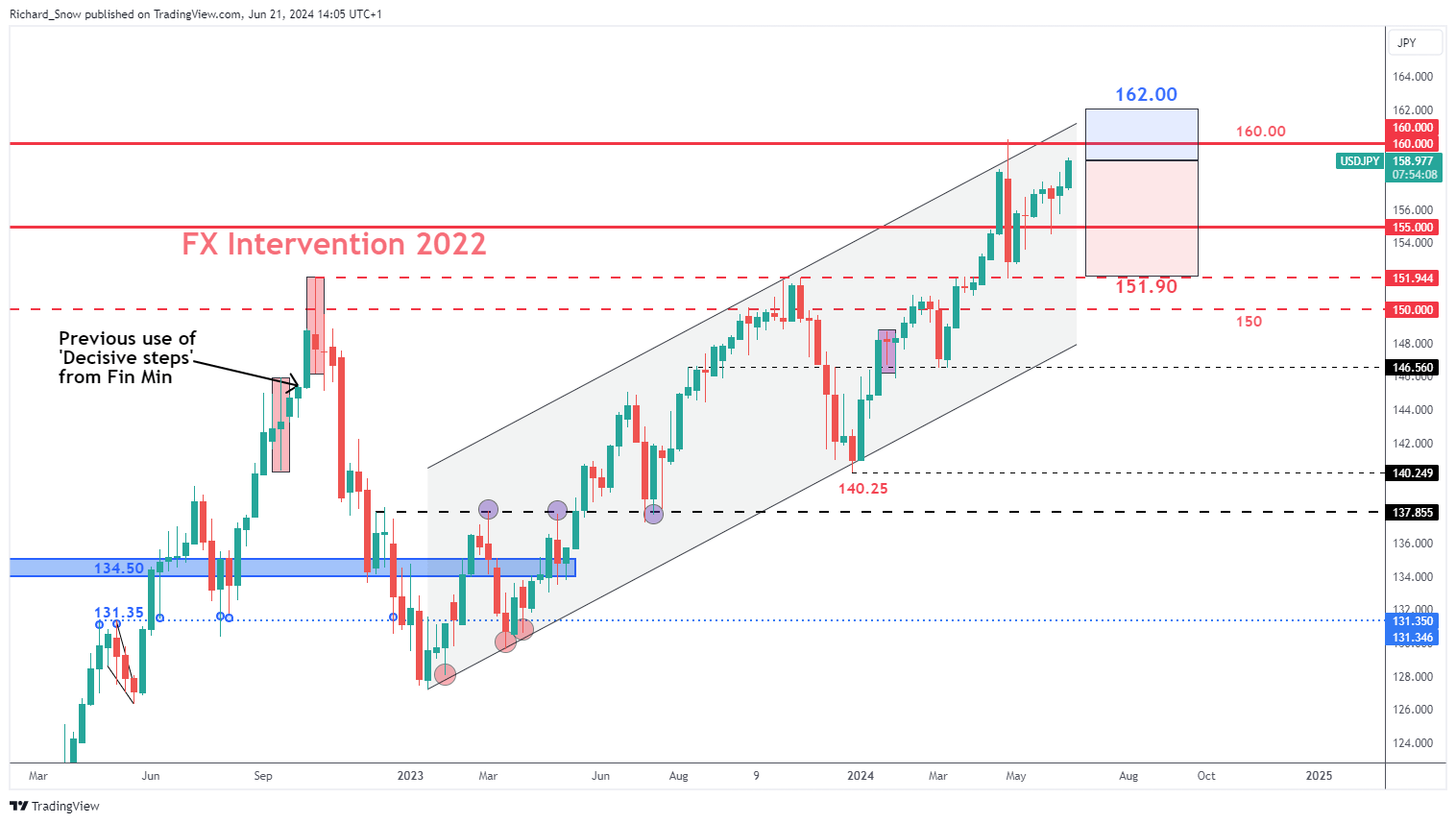

USD/JPY Back in Focus as Intervention Risks Return

The Bank of Japan (BoJ) disappointed the markets when it met in June, delaying details of the much-anticipated plans to lower government bond purchases in its next phase of policy normalisation. Lowering the quantity of bonds purchased each month should allow Japanese bond prices to ease, elevating bond yields in the process and providing some support for the beleaguered yen .

In any case, the wide interest rate differential between the US and Japan is really what is working against the yen. The rapid yen appreciation that followed April’s FX intervention has all been lost. USD/JPY pushes on towards 160.00 again and although it has approached the significant marker in a less volatile manner, the consistent depreciation of the yen will concern currency officials.

It was hoped that the disappointing economic growth in the US for Q1, coupled with encouraging progress in inflation, would mark the start of a slowdown causing the Fed to contemplate lowering rates which would help to reduce the rate differential. On the other side of the equation, the BoJ has been searching for further opportunities to bridge the rate gap by hiking interest rates, but the preconditions around wages and inflation are yet to convince officials to alter rates in a meaningful way. However, with the Fed staying put and the BoJ implementing one inconsequential hike, USD/JPY took the familiar path of least resistance.

USD/JPY has limited upside from 160.00 if recent history is anything to go by. The country’s top currency official, Masato Kanda also felt the need to clarify in June that there is no limit to the resources available for currency intervention. In Q3, the threat of more FX intervention by Japanese officials and the possibility of a more dovish Fed suggest that USD/JPY is likely to head lower at the end of the quarter. Therefore, the most imminent level to the downside appears at 155.00 with momentum potentially extending to 151.90 – the level corresponding to the round of FX intervention that took place in October 2022.

USD/JPY Weekly Chart

Source: TradingView, prepared by Richard Snow